Introduction

This submission outlines the cost of living pressures that are facing Western Australians, with a focus on the areas of housing, transport, food, energy and water. It also provides insights from the WACOSS and Bankwest Curtin Economics Centre Understanding Utility Hardship report, and the WACOSS and UnionsWA Low Pay Report.

Despite Western Australia’s strong economic position and high performing job market, the combination of minimal or stagnant wage growth and persistently insufficient Commonwealth income support, has meant that many households are struggling to cover the cost of basic necessities. Significant and sustained price increases erode the purchasing power of their income.

The lack of available rental properties across Western Australia has seen rents continue to skyrocket, with outdated tenancy legislation leaving renters disempowered and subject to the whims of landlords and real estate agents. In May 2022, the Reserve Bank of Australia increased interest rates for the first time in eleven years and they have continued to rise since. War in Ukraine, floods in the Eastern States, and corporate profiteering, meant that the costs of fuel and groceries, as well as many other household items, soared.

The WA Government has taken necessary actions to keep the household fees and charges set by government at or below CPI. With indexation at such high levels, however, and many of the most substantial costs borne by households not set directly by government, more support from the Commonwealth and State Governments will be needed for Western Australian households to be able to meet their living costs at this time.

It is hoped that the recently passed amendments to the Fair Work Act that make critical improvements to the bargaining power of workers will result in wages increasing. For those locked out of the paid workforce, however, there are no current commitments to meaningfully increase the rate of JobSeeker and other associated payments.

Housing

Access to safe, secure and affordable shelter is essential for people to be able to fully engage in our community. Stable tenancies are crucial to support positive outcomes in areas like health and wellbeing, education and employment. Conversely, insecurity and instability in housing creates the circumstances for increased hardship and entrenched disadvantage.

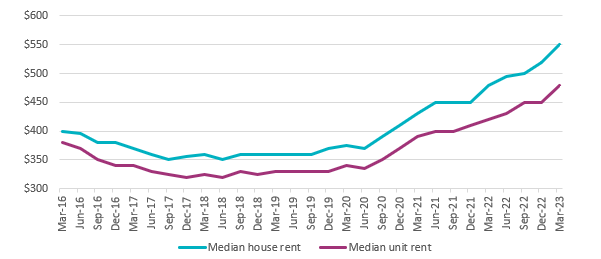

Housing is the single largest living cost for households in Western Australia. Housing costs have a disproportionate impact on those living on the lowest incomes.[1] With median rents in Perth on the increase since 2018 and drastically rising since 2020, the pressure rental costs place on households has never been more apparent. As of March 2023, median house rents in Perth had increased over the past 12 months by more than 14.5 per cent and by nearly 28 per cent since March 2021. Median unit rents have increased by 14.3 per cent since 2022 and by 23.1 per cent since 2021.[2]

Perth Median Rents

Source: REIWA data

The increasing lack of affordable rental properties in Western Australia is reflected in the latest Rental Affordability Index results. Perth’s rental affordability index score declined to its lowest level since 2016, with a drop of 15 per cent over the past two years. Over the past year, regional WA saw a decline of 8 per cent in its rental affordability index score. Rent as a share of income for a single person on JobSeeker was calculated to be 111 per cent in Greater Perth and 110 per cent in the rest of Western Australia.[3]

It is important to recognise that this is an exacerbation of what was already a profoundly fraught situation for those on the lowest incomes. Even during the period between 2015 and 2018, when median rents had declined from where they had been during the mining boom, the WA Housing Industry Forecasting Group had noted that ‘for those on the lowest incomes, conditions have not changed.’[4] When growth in housing supply occurs in the mid-to-high price segments, it does not necessarily create a ‘trickle-down’ effect into the low price segments by freeing up established housing stock.[5] As such, targeted intervention to support those on the lowest incomes access housing, including through increasing income support and constructing public housing, is needed.

The very low level of accessible properties available to rent for households receiving government payments and for single minimum wage earners, including single parents, strongly indicates the likelihood that many of those households will be living in housing stress or making do with housing that is not appropriate for their circumstances. Fewer appropriate and affordable housing choices often means that low-income households are being forced onto the fringes of the metropolitan region in order to find housing, placing them further away from jobs, schools and services and adding an even greater strain on the weekly travel budget.

The more of their income that households must dedicate to covering housing costs, the less they will be able to spend on other essentials like food, energy and health. It can also mean that any slight increase in their rent can have a dramatic impact on their ability to stay in a property and maintain the important connections they have established throughout their local community, along with their proximity to jobs and services.

Transport

The high price of fuel, inflation and car loan repayment costs have all contributed to transport having an increased negative impact on household budgets. As of September 2022, transport costs were found to take a 13.6 per cent bite out of the typical household income in Perth. The annualised cost of transport in Perth was $19,814. In Bunbury, transport costs were found to make up 14 per cent of a typical household income, positioning it as the fourth most unaffordable regional centre for transport costs in Australia.[6]

A lack of affordable, accessible transport can contribute to locking people out of the labour force. 17 per cent of the participants in the 100 Families WA study reported that was a barrier for them to gain employment.[7] The Western Australian State Government has made significant strides in improving the affordability of public transport for households in outer-suburban areas by capping fares at the cost of a two-zone journey and is investing strongly in expanding the metropolitan train network. Households in outer suburban and regional areas where public transport options are limited or not present, however, remain particularly dependent on access to cars as the primary form of transportation.

State car registration costs can contribute to the inaccessibility of transport, creating additional hurdles for those who are unemployed to secure employment in industries that require them to have access to a car. The introduction of a monthly payment option in Western Australia from 27 September 2022 was a welcome step in assisting households manage their finances, but will not reduce the burden that car registration payments place on their limited income.

In 2021, the Salvation Army reported a 90 per cent increase in requests for assistance to pay car registrations in WA.[8] Uniting WA and Anglicare’s Emergency Relief and Food Access Service have also seen a rise in demand for car registration payments. With only a select number of emergency relief providers able to pay for car registration payments, those few that do are often overwhelmed with demand.

Food

Low income is the strongest and most consistent predictor of food insecurity. Food insecurity is the state of being without regular access to a sufficient quantity of safe, nutritious food to meet an individual or household’s nutritional needs. It often corresponds with lower access to other basic needs, such as safe and affordable housing and secure employment as well as increased use of healthcare.

Increases in food prices have had a significant impact on household budgets. According to the UBS Evidence Lab Grocery Study, Woolworths prices increased by 4.3 per cent in the first quarter of 2022, while Coles’ prices grew by 3.2 per cent.[9]

Food manufacturer SPC raised the prices of 100 Australian staple food items, such as baked beans and spaghetti, canned tomatoes and fruits, by as much as 20 per cent.[10] The West Australian examined a broad range of grocery items commonly purchased by consumers and found the total cost had jumped from $90.26 in 2019 to $141.68 in 2022, equating to an increase of 57 per cent.[11]

Foodbank reported in 2022 that over the past 12 months, 280,000 households in Western Australia had gone hungry as a result of insufficient income, including skipping meals or not eating at any point throughout the day. Further, over 116,000 children were living in severely food insecure households in WA.[12]

WACOSS member organisations providing food relief reported that there has been a significant recent increase in people requesting emergency food relief across the state.

“Vinnies are witnessing unprecedented demand for food relief and has seen a significant increase in requests for food support over the last few years. From 30,000 people in 2017-18 to 45,000 in 2019/20 to an estimated 60,000 plus people in 2021/22. Our capacity is limited to 55,000 people for food relief based on existing resources. In real terms and referrals, our actual need is around 110,000 across the state.

At the moment Vinnies is doing around $100,000 a month in Food Cards and around $100,000 worth of food in donated hampers. An increasing area of concern is people who are homeless, living in caravan parks or crashing with other families, which is tied up in the ongoing and increasing cost of housing.”[13]

These anecdotes are corroborated by the findings of Foodbank’s 2022 Hunger Report, with 23 per cent of those surveyed nationally reporting they were unable to afford food more often than in the previous year. Increased food and grocery costs was cited by 49 per cent of survey respondents as a contributor to their food insecurity, followed by increased energy costs, including fuel, by 42 per cent and housing costs by 33 per cent.[14]

Energy and Water

Western Australia is in the advantageous position that ownership of our electricity and water retailers for residential consumers has remained in the hands of the public. Residential customers have largely been shielded in those areas from the failure of privatisation over east, with the supposed benefits of competition remaining elusive. The retail gas market in Western Australia, however, was made fully contestable in 2004. Prices for small-use customers, such as residential households, in the Mid West/South West, Kalgoorlie Boulder and Albany supply areas are still subject to a regulated price cap set by the WA Government.

Public ownership of electricity and water, coupled with a strong regulatory regime means that it is possible to pursue positive social outcomes to ensure equitable and affordable access to utilities that would be impossible to achieve were the provision of these services left subject to the profit-motive alone. Despite this, there are many Western Australian households for whom utility hardship is a lived reality and significant concern.

The 2022 Understanding Utility Hardship report by WACOSS and Bankwest Curtin Economics Centre provides rich insights into the causes and experiences of how utility costs can contribute to financial hardship for Western Australians. The report utilised a mixed methods approach that included qualitative focus group and interview data of financial counsellors, quantitative survey data of Water Corporation customers, and quantitative data sets provided by the Financial Counsellors Network.[15]

We consider that utility hardship can be understood as the lack of affordable, reliable and adequate energy and water services. This hardship presents in three intersecting and overlapping forms. These are:

- Difficulty paying utility bills;

- Restricting utility usage to the detriment of health and wellbeing; and

- Having a relatively low income and spending a relatively high proportion of income on utility costs.

That first form is typically the most visible as it is where customers are more likely to interact and engage with utility retailers and financial counsellors. For most households experiencing utility billing hardship, utility bills are unlikely to be their largest cost burden unless they have accumulated significant utility debt and debt recovery costs. Housing, followed by food and beverages, are consistently the most significant costs facing households on a day-to-day basis. Due to how people prioritise their spending though, this may present as utility hardship.

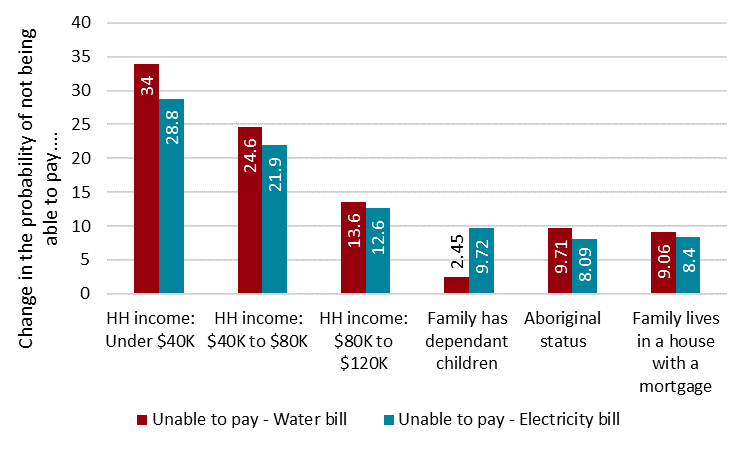

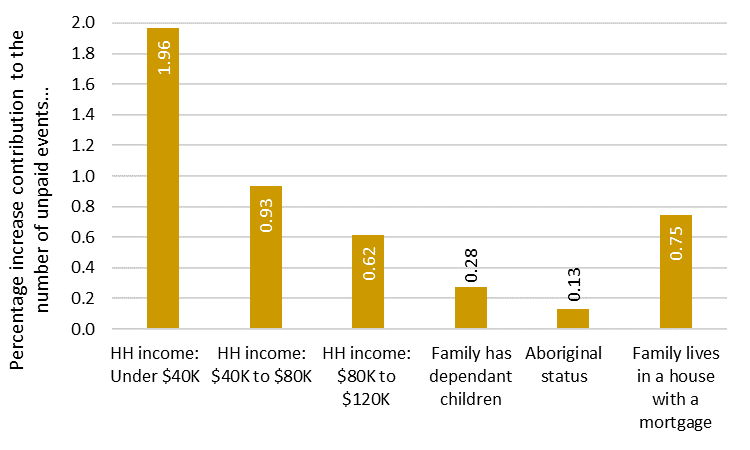

The Water Corporation Customer Survey provided insights into the contributors of utility stress and hardship. Unsurprisingly, income was found to be the largest contributing factor to utility hardship. The lower the income, the higher the probability of being unable to pay water or electricity bills. Having dependent children also increases the probability of having unpaid bills, and this probability is higher for electricity bills than water (9.7 per cent vs 2.4 per cent). Aboriginal and Torres Strait Islander status, as well as having a mortgage, are significant contributors to utilities hardship (averaging 9 per cent).

Contributors to households’ inability to pay for bills, household characteristics

Source: Bankwest Curtin Economics Centre | Water Corporation Customer Survey.

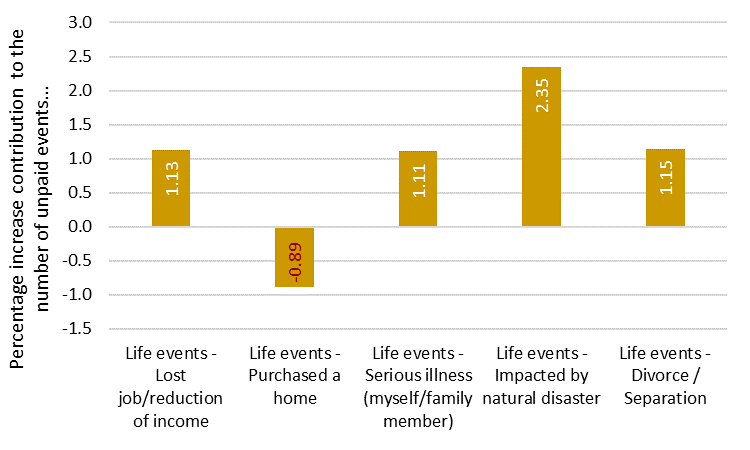

Natural disasters, losing a job or having a decline in income, and serious illness were the most significant life events that contributed to utility hardship for many respondents. A significant correlation was observable between defaulting on different bill payments. Not being able to pay for electricity was the best predictor of people’s ability to pay their water bills, with the best predictor for electricity being unable to pay for water and gas. Being unable to make mortgage repayments was also found to be a strong predictor of utility hardship. Households that cannot access from their savings or raise $4,000 in a week for an emergency are on average 50 per cent more likely to be unable to pay their electricity or water bills than households that could.

Contributors to household’s inability to pay for bills, life events

Source: Bankwest Curtin Economics Centre | Water Corporation Customer Survey.

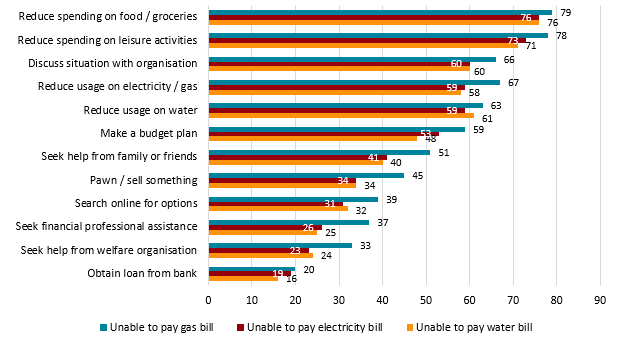

Reducing spending on food and groceries was the most common strategy utilised by respondents in order to cope with being unable to pay their utility bills, with 76 per cent of those who were unable to pay their electricity bills and water bills, and 79 per cent of those unable to pay gas bills indicating that this was a strategy they would likely use. This was closely followed by reducing spending on leisure activities.

Coping mechanisms by type of utility bill unable to be paid, %

Source: Bankwest Curtin Economics Centre | Water Corporation Customer Survey.

When other bills are also considered, such as insurance payments, credit card bills, loans, mortgages and rents, a similar pattern in coping mechanisms that respondents indicated they were likely to utilise is observable. Even if after dividing those bills between what could be considered discretionary or essential, reduction in spending on food and groceries, closely followed by reduction in spending on leisure activities were identified as the most likely strategies that respondents who had been unable to pay a bill within the last year would utilise.

60 per cent of those who were unable to pay their electricity and water bills indicated they would likely discuss their bill and what options might be available with the utility retailer, and 66 per cent of those unable to pay gas bills would do the same. A similar percentage indicated that they would resort to strategies involving reducing their consumption of water, electricity or gas in order to cope.

Notably, approximately 10 per cent more of those unable to pay their gas bills indicated they would seek professional financial assistance or help from a welfare organisation than those unable to pay their electricity or water bill. This may indicate a gap in the assistance that is provided by the gas retailers, requiring those customers unable to pay their bills to seek assistance from other avenues.

In interviews, financial counsellors were asked to reflect upon the difference between utility hardship programs, for example between water, electricity or gas, and how they compare to one another. They noted a clear distinction between publicly-owned and privately-owned utility companies and how they differed in services offered and approach to customers in hardship. The publicly-owned utilities went beyond the minimum support that was required under the Consumer Codes, while the gas companies did not.

Financial counsellors highlighted how publicly-owned utilities, such as water and electricity, often reduce the amount of the outstanding debt for a hardship customer if they maintain a payment plan, as well as engage in case management techniques where cases are assessed on an individual basis by a dedicated case manager. Counsellors also noted that Water Corporation and Synergy have developed a strong relationship with the financial counselling sector, allowing them to adjust and tailor their hardship programs and approaches with clients.

Financial Counselling Data

While there is a broad range of people accessing financial counselling services, people in entrenched disadvantage due to persistent low incomes, low-waged workers and households, people experiencing an adverse life event, or people with multiple large loans were identified as four key demographic cohorts in financial hardship.

Clients of the Financial Counselling Network were found to have higher rates of energy hardship than water hardship, with the prevalence of people citing electricity bills as an issue being twice as much as that of water bills. Alongside financial hardship, mental health and other health issues were found to be the two largest co-occurring issues for financial counselling clients. Employment issues and factors related to domestic violence, parenting and family issues, separation and divorce and child support, were also significant co-occurring issues for financial counselling clients.

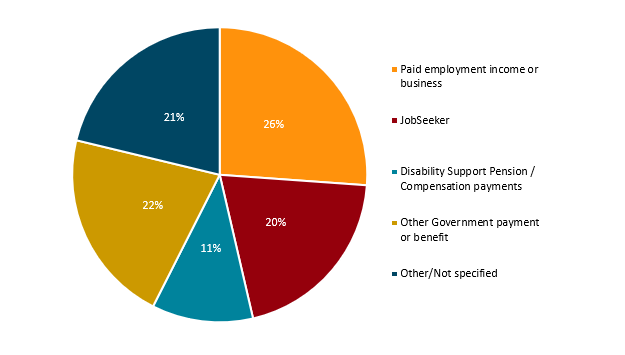

Main source of income, FCN

Source: Bankwest Curtin Economics Centre | Financial Counselling Network data 2022.

FCN data also reveals the main source of income for people experiencing financial hardship and accessing their services. Even though people in government payments such as JobSeeker, disability support pension or other government payments make up the majority of FCN clients, more than a fourth of FCN clients have paid employment income or income from a business. Out of all government payments, a fifth of FCN clients are JobSeeker recipients, thus making it a strong predictor of financial hardship.

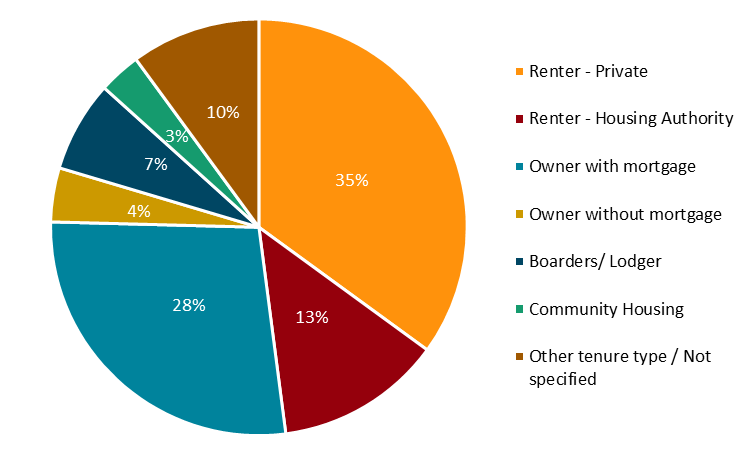

Home ownership type, FCN

Source: Bankwest Curtin Economics Centre | Financial Counselling Network data 2022.

Unlike the Customer Survey respondents, who were predominantly home owner-occupiers, FCN clients are from a wide variety of housing arrangements. 35 per cent of clients are private renters, followed by owners with a mortgage, at 28 per cent, and renters from the housing authority at 13 per cent. These findings demonstrate that people living in rental housing are at higher risk of financial hardship, making up almost half of the households seeking help from the FCN.

Fortnightly expenditure patterns, FCN

Source: Bankwest Curtin Economics Centre | Financial Counselling Network data 2022.

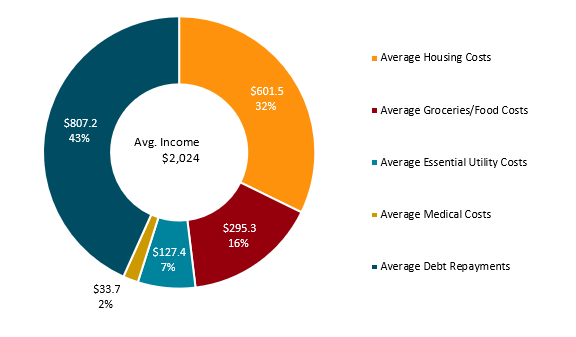

In order to assist clients with money management, budgeting and prioritising financial goals, the FCN collects data on selected expenditure patterns of families in family hardship. Clients’ average fortnightly income is $2,024, which varies according to household suburb. It can be as low as $980 per month for families living in Belmont and as high as $3,300 for Joondalup and Success; this is not the average suburb income but the average income of FCN clients from those suburbs.

While housing costs represent just over a third of the overall household’s expenditures (32 per cent), average debt repayments represent an enormous 43 per cent of household’s expenditure at $807 per fortnight. This is $200 more per fortnight more than what they pay for their housing, which is usually a household’s highest expenditure item.

Utility costs are 7 per cent of household expenses and represent on average a $130 expenditure per fortnight. When all basic fortnightly expenses are added, the total comes to $1,865.10, leaving just $158.90 per fortnight from the average income for other costs, such as education, recreation, clothing, or emergency situations. The suburbs where households have the higher deficits in expenditure relative to income are Gosnells, Osborne Park, Coolbellup and Yanchep.

Reasons for accessing FCN services

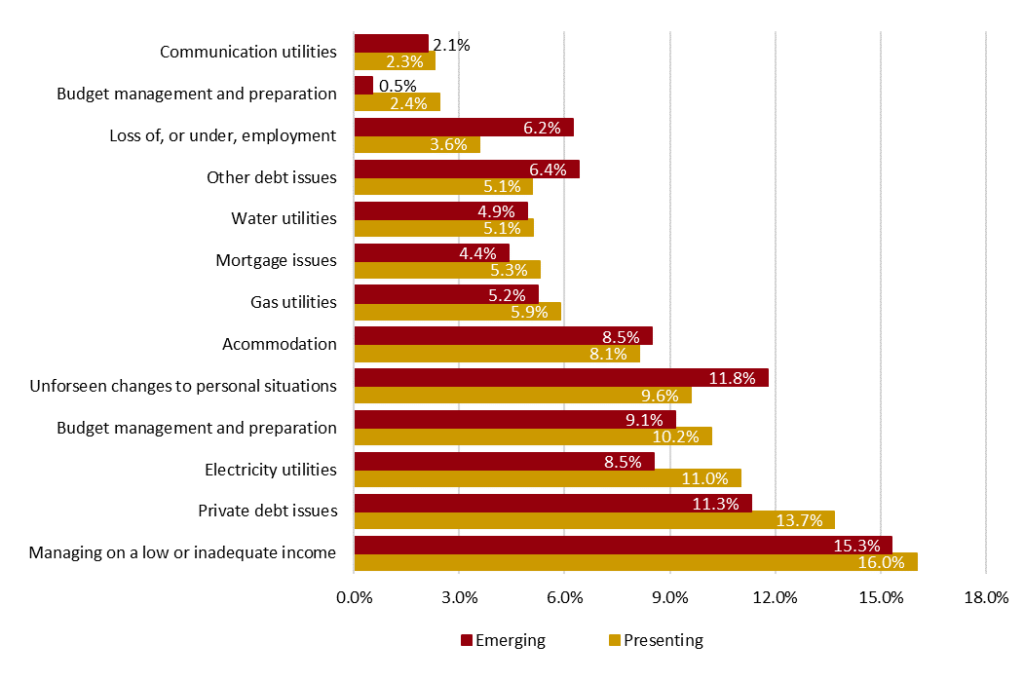

Source: Bankwest Curtin Economics Centre | Financial Counselling Network data 2022.

Note: ‘Presenting’ reasons are those that the client presented with or disclosed during the initial intake into the service, while ‘emerging’ reasons are those that emerged during subsequent meetings or assessments by the financial counsellor.

The two main reasons that people access FCN services are when people are managing on a low or inadequate income or are having private debt issues. Experiencing utility hardship is also an important reason, with issues with electricity bills ranking as the third highest reason that people access FCN services, issues with gas bills ranking seventh and issues with water bills, ninth. FCN clients suffer from energy hardship more significantly than they do from water hardship, with the prevalence of people citing electricity bills as an issue being twice as much as that of water bills. This may be due to the higher proportion of renters in the sample that potentially do not pay for water bills.

There are often a number of complex co-occurring health, social or relationship issues faced by people experiencing vulnerability and financial hardship. The two largest co-occurring issues for FCN clients are mental health and other health-related issues.

Other factors correlated with financial difficulties include domestic violence, parenting and family issues, separation and divorce and child support issues. There are also factors related to alcohol and substance abuse or legal issues such as imprisonment. Finally, there are contributors that are not often considered when evaluating financial hardship such as social isolation and social disconnection.

Co-occurring issues with financial hardship, FCN

Source: Bankwest Curtin Economics Centre | Financial Counselling Network data 2022.

Low Paid Workers

The 2022 Low Pay Report by WACOSS and UnionsWA demonstrated that workers on low wages in Western Australia do not consider that their wages are increasing by the same proportion as their living costs, placing them in a state of financial stress or hardship. [16] 66.3 per cent of respondents with an annual household income before tax that was lower than $52,000 reported that they had $100 or less a week after meeting their essential costs. 34.3 per cent reported that they had $50 or less a week after meeting their costs each week, which was the highest response for that income group.

Low-waged workers also reported the highest percentage of respondents falling behind into debt, at 15.4 per cent. Approximately 39 per cent of low-waged respondents identified that their income just met their cost of living. Many workers reported that they had no emergency savings safety net, were accessing savings or superannuation funds to cope with financial hardship or are worried about not having enough to finance retirement. Just 6.9 per cent of respondents in the low-wage category indicated that they were currently coping well.

The report further examined the disposable income and financial stress levels of just those respondents who reported an annual household income lower than $52,000, against those in that income bracket who were also in full-time employment.

Disposable income after essential costs for households with annual income lower than $52,000

| All employees | Full-time workers only | |

| Under $100 | 66.3% | 61.9% |

| $100 – $200 | 32% | 21.4% |

| $200 – $500 | 21.3% | 16.7% |

| More than $500 | 3% | 0% |

| Total no of respondents | 169 | 42 |

Financial stress levels for households with annual income lower than $52,000

| All employees | Full-time workers only | |

| I/we are falling behind into debt | 15.4% | 15.9% |

| My/our income just meets costs of living | 38.9% | 40.9% |

| I/we have a bit of disposable income after meeting costs | 28.6% | 29.5% |

| I/we are able to have a decent disposable income and save as well | 10.3% | 9.1% |

| I/we are comfortable with few financial concerns | 6.9% | 4.5% |

| Total no of respondents | 175 | 44 |

Source: Eva Perroni and Graham Hansen (2022) Low Pay Report

What this comparison indicates is that for those workers who are earning a low wage, access to full-time work is not in itself a guarantee that workers will earn enough to cover their basic needs or to avoid financial stress, hardship or debt. The fundamental problem is that the income of these workers is simply too low to meet cost-of-living expenses or to provide some discretionary income.

To ascertain how Western Australian households are coping financially, the survey included the open-ended question “In your own words, how are you or your household coping financially”.

Respondents’ testimonies described a variety of hardships that they experienced in trying to survive on their low wages. Workers across all employment categories – full-time, part-time and casual – indicated the hardships of living on low wages. These included inadequate income to meet weekly or fortnightly basic living costs, an inability to save, difficulty in repaying debt, and a need to continually adjust future plans, expectations, and dreams. Many low-waged workers self-reported that they are ‘struggling to make ends meet’, are living pay cheque to pay cheque or are on the precipice of financial precarity and/or falling into debt.

- “I’m just trying hard to survive from one fortnight to the next without incurring any big debts”

- “I cannot think or plan too far ahead. I am constantly worried about having to dip into savings that I would like to use for a house if that was ever going to be possible”

- “Struggling every week to make ends meet, can’t even save a couple of dollars”

- “Wage just covers cost of living – utility bills, insurances, rates, car, food, medical, phone, etc. I am unable to save, live pay to pay, and have been unable to get out of credit card debt, stuck on $4,500 overdraft. So financially just keeping my head above water, just”

- “We run out of money a few days before pay day every time”

Low-income workers indicated that they are struggling to afford the rising costs of necessities, while emphasising that their wages are not increasing by the same proportion. Sharp increases in the cost of living, particularly food and fuel, are contributing to especially acute feelings of financial stress, straining low-waged workers’ already tight finances. Many respondents indicated that they are sacrificing regular and important items in their households’ budget in order to compensate for the rising costs of basic necessities.

- “We are struggling, rising costs and lower wages are not improving so we are robbing Peter to pay Paul”

- “We barely scrape by. Any increases to rent/food/utilities will see us slowly subsiding into a pit of debt we would never recover from. Wages are not increasing at the same rate”

- “We are OK… as my partner and I are still working. However, cost of living is going up. Groceries are more expensive, as is fuel. We have the same income however more outgoing costs. We have had to make a lot of adjustments in order to get by”

- “Just managing, bills seem to increase electricity, water and health insurance for example but wages aren’t increasing at same rate. We are seriously looking at dropping health insurance which then puts more pressure on public health”

Low-income workers indicated that they are struggling to afford the rising costs of necessities, while emphasising that their wages are not increasing by the same proportion. Sharp increases in the cost of living, particularly food and fuel, are contributing to especially acute feelings of financial stress, straining low-waged workers’ already tight finances. Many respondents indicated that they are sacrificing regular and important items in their households’ budget in order to compensate for the rising costs of basic necessities.

The fundamental power imbalance between individual workers and employers is why it is critical that we have safety nets like the minimum wage and award pay rates. In order to ensure workers are being paid enough that they are able to meet the cost of living, minimum wages must be set at an adequate level. Governments have a clear role in this, not only by creating the necessary legislative conditions to ensure workers are paid liveable wages, including protecting workers from wage theft, but also as significant employers themselves and contractors of services.

To address issues contributing to pay being insufficient, there is also a clear need for unions to be able to freely organise in workplaces and take industrial action when needed. As the frontline against injustice in the workplace, through delegates, shop stewards and the broader membership, unions provide a direct means for protecting conditions and pushing for higher wages.

Endnotes

[1] ACOSS/UNSW Poverty and Inequality Partnership, Poverty, Property and Place: A geographic analysis of poverty after housing costs in Australia, City Futures Research Centre & the Social Policy Research Centre (Report, 2020).

[2] REIWA, Perth property market (2023).

[3] National Shelter, the Brotherhood of St Laurence, and SGS Economics and Planning Rental Affordability Index (Report, 2022).

[4] Housing Industry Forecasting Group, Forecasting Dwelling Commencements in Western Australia 2017-2018 (Report, 2017).

[5] Rachel Ong, Tony Dalton, Nicole Gurran, Christopher Phelps, Steven Rowley and Gavin Wood, Housing supply responsiveness in Australia: distribution, drivers and institutional settings, Australian Housing and Urban Research Institute (Report, 2017).

[6] Australian Automobile Association, Transport Affordability Index Quarter 3 2022 (Report, 2022).

[7] Ami Seivwright and Paul Flatau, Insights into hardship and disadvantage in Perth, Western Australia: The 100 Families WA Baseline Report. The 100 Families WA project (Report, 2019).

[8] Josh Zimmerman, ‘The Salvation Army pays car registrations for homeless West Australians’, The West Australian (2021) thewest.com.au/news/social/the-salvation-army-pays-car-registrations-for-homeless-west-australians-ng-b881889193z

[9] Holly Hales, ‘Reason for hike in Australian grocery prices revealed’, The West Australian (2022).

[10] Ronald Mizen, ‘Baked beans, spaghetti up 10-20pc as inflation bites’, Australian Financial Review (2022).

[11] Cheyanne Enciso, ‘Cost of living: The shock increase in total cost of a grocery shop since 2019 revealed.’ The West Australian (2022).

[12] Foodbank, Hunger in Australia – The Facts (Web Page, 2022).

[13] WACOSS/St Vincent de Paul Society (WA), email correspondence, 22 April 2022.

[14] Foodbank WA, Hunger Report (Report, 2022).

[15] Graham Hansen, Eva Perroni and Dr Silvia Salazar, Understanding Utility Hardship, Western Australian Council of Social Service and Bankwest Curtin Economics Centre (Report, 2022).

[16] Eva Perroni and Graham Hansen, Low Pay Report 2022, Western Australian Council of Social Service and UnionsWA (Report, 2022).